US Stocks Higher on Rising Rate Cut Bets

Stocks Pushing Higher

US equities are on course to end the week higher amidst the dovish repricing in the Fed rates outlook which is helping bolster risk sentiment this week. The S&P is grinding higher on the back of yesterday’s ADP jobs data which printed -38k vs 7k expect, down from 42k prior. The data, which will be the last labour market input ahead of the FOCM next week, has helped cement rate cut expectations. The CME group is pricing an 87% chance of a cut next week.

Core PCE Tomorrow

Looking ahead, tomorrow’s core PCE data will be the final tier one data for the week. Expected unchanged at 0.2% MoM, the data should have little impact on rate expectations. However, if we see any downside surprise tomorrow, this should see rate cut pricing creeping higher again putting further pressure on USD into the FOMC next week.

Data Next Week Ahead of FOMC

Ahead of that meeting the JOLTs jobs number on Tuesday will be the final data to watch. Again, any fresh weakness should help keep USD well sold and stocks bid into the FOMC while it would likely take a meaningful upside surprise to dilute easing expectations at this juncture. If we do see an upside surprise, however, there is an outside chance that the Fed might opt to wait for the October and November NFP reports on the 16th. This would likely cause a sharp reactive move higher in USD if seen, causing a sharp correction lower in equities. As such, plenty of volatility risk to navigate around the FOMC next week.

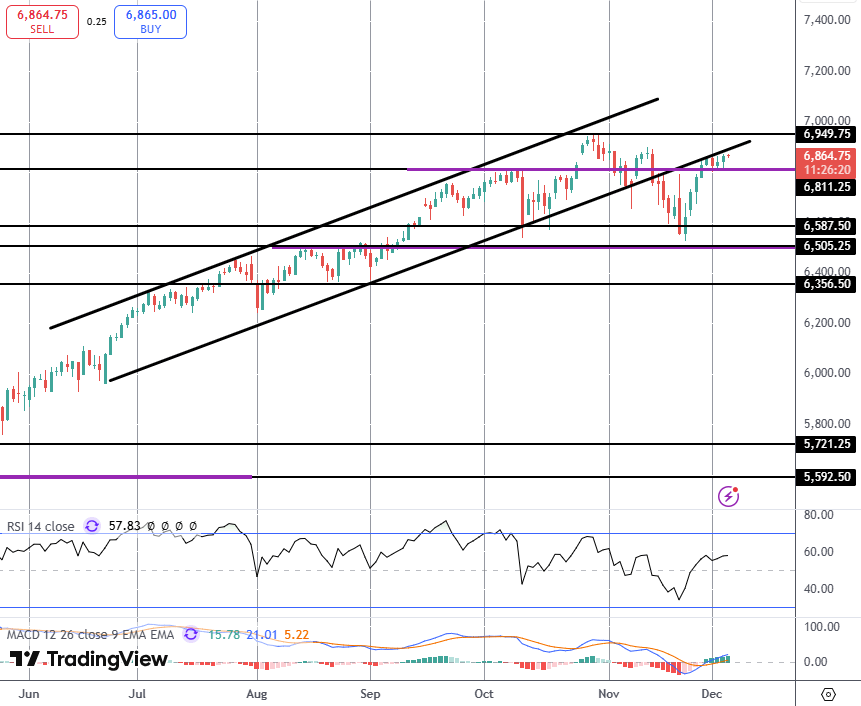

Technical Views

S&P 500

The rally in the S&P has seen price climbing back above the 6,811.25 level, now retesting the underside of the broken bull channel. With momentum studies climbing, focus is on a fresh push higher with the YTD highs around 6,949.75 the next objective for bulls. To the downside, 6,587.50 remains key support to watch.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.