Institutional Insights: JPMorgan Delta One Flows & Positioning 7/7/26

JPM Delta-One Flows & Positioning — Trading Takeaways

Memory still the only game in town; geo-hedge unwind continues

The flow picture remains narrow but powerful: investors are still paying up for Memory/Semis/AI infrastructure, while continuing to unwind Energy, Materials, Precious Metals, and geopolitical hedges. Sector rotation is clearly moving out of cyclicals tied to commodities and into Discretionary, Tech, Financials, Healthcare, and Staples.

ETF data remains noisy due to Russell rebalance/CIB distortions, particularly in Growth/Value factor flows, but the underlying message is consistent: risk appetite is intact, but increasingly selective.

1. Stay long Memory/Semis vs. broad AI thematic baskets

DRAM/RAM funds took in +$2.3Bn, confirming that investors are expressing AI demand through hardware bottlenecks and memory supply chains, not generic AI wrappers.

Action:

Prefer Memory/Semis exposure over broad AI thematic ETFs.

Long Memory/Semis vs. short broad AI thematic baskets remains the cleaner relative-value expression.

Watch for continued inflows into Tech sector ETFs as confirmation.

2. Fade geopolitical hedge proxies: Energy, Gold, broad Commodities

Commodities saw another week of outflows, with Energy -$0.8Bn, Materials -$0.4Bn, and Precious Metals -$0.9Bn, mostly gold. The market is clearly de-risking the geopolitical hedge trade.

Action:

Stay cautious on Energy and Materials near term.

Continue to fade rallies in Gold/Precious Metals unless real yields or USD turn materially supportive.

Commodity beta remains vulnerable while hedging demand fades.

3. Equity rotation broadening, but leadership still Tech-heavy

Equity ETFs saw +$20.3Bn of inflows, led by the US and International DM. Sector inflows were strongest in Discretionary, Tech, Financials, Healthcare, and Staples, all above +1z.

Action:

Favor barbell equity exposure: Growth/Tech plus defensive compounders in HC/Staples.

Discretionary inflows suggest the consumer trade is not dead, but selectivity matters.

Financials inflows support continued rotation into rate-sensitive/value-adjacent cyclicals.

4. Fixed Income inflows are strong, but futures positioning says caution

Fixed Income ETFs saw +$16.1Bn, a strong +1.2z week. Inflows were led by Long-term government bonds, IG Corporates, and Aggregate/Multi-sector funds. But futures showed large selling in UST Ultra 10y and Korea 10y, while CTAs likely remain short global fixed income.

Action:

ETF buyers are adding duration, but systematic/futures positioning remains bearish.

Prefer IG credit and aggregate bond exposure over aggressive duration longs.

Long-end duration still needs confirmation from macro data or rates momentum.

5. Crypto outflows remain a clear negative signal

Crypto ETFs saw -$0.5Bn, marking an 8th consecutive week of outflows, with Bitcoin continuing to lag.

Action:

Avoid chasing crypto beta until flows stabilize.

BTC underperformance remains a warning sign for speculative risk appetite.

Any bounce likely needs ETF flow reversal to be sustainable.

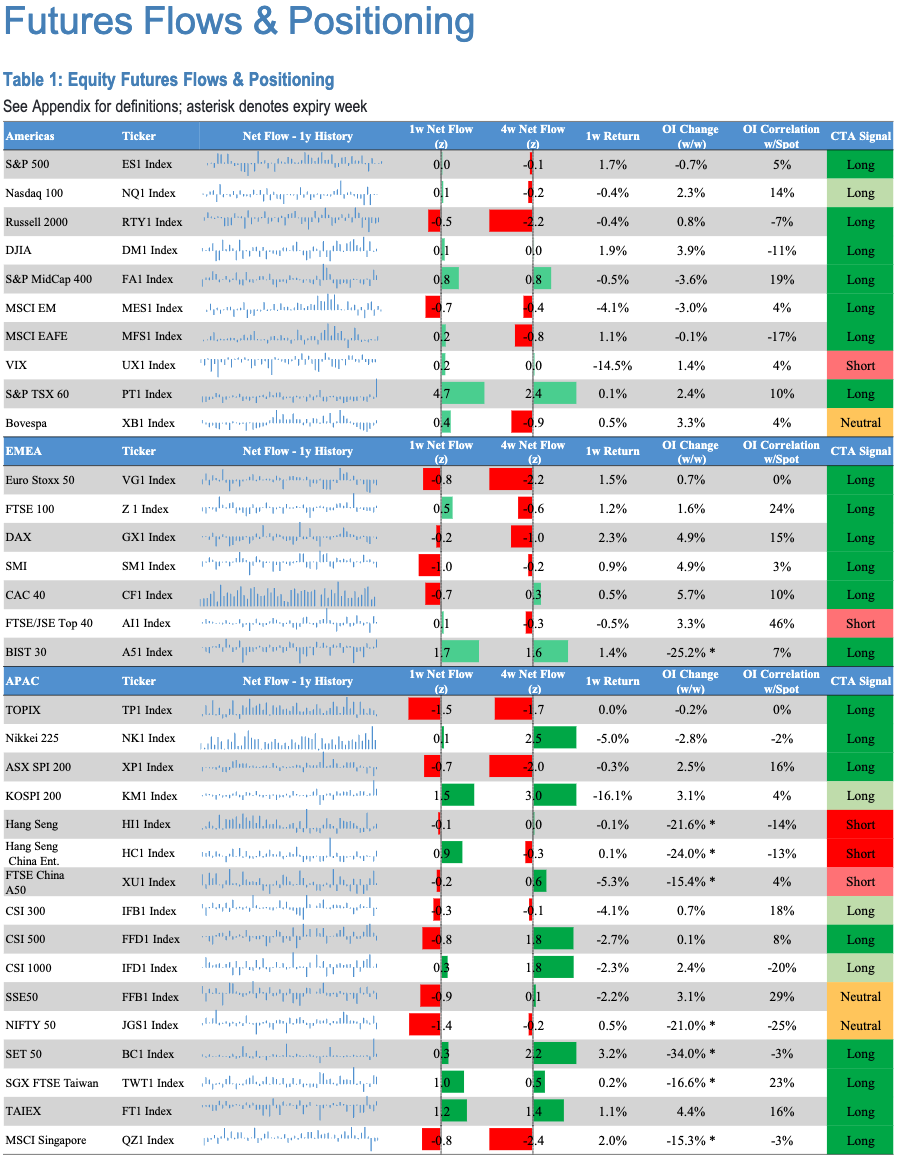

6. Futures flows flag regional divergence

Large net buying appeared in S&P/TSX 60 and BIST 30 futures, while large selling hit UST Ultra 10y, Korea 10y, and JPY futures.

Action:

Canada and Turkey futures flow momentum looks supportive short term.

JPY selling remains aligned with bearish yen momentum.

Korea duration selling is a notable local rates pressure point.

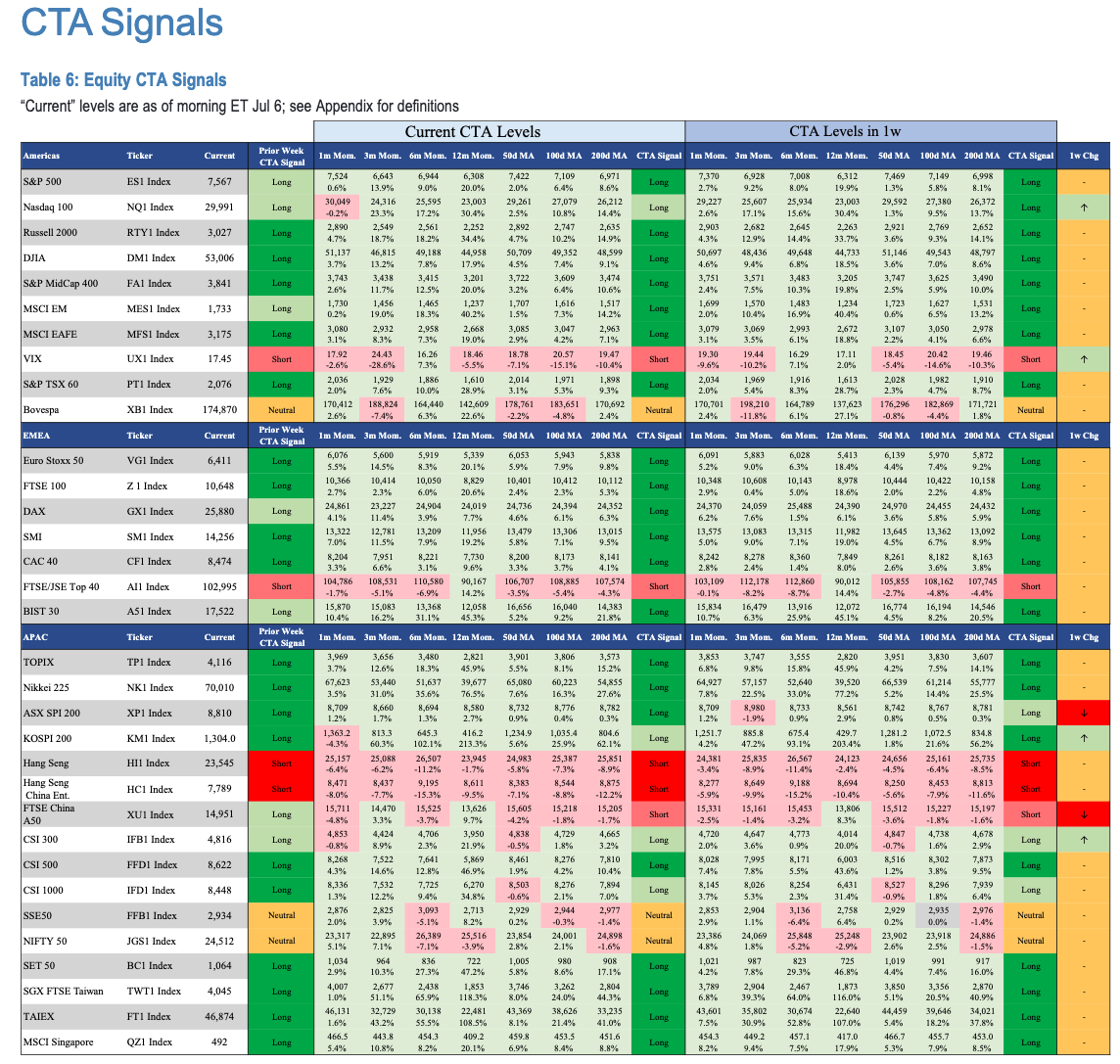

7. Asset Managers rotating out of SPX into NDX/MID

CFTC data shows Asset Managers reducing SPX exposure while adding to NDX and MID futures. Leveraged Funds increased shorts in NDX and RTY, while cutting shorts in EAFE and VIX.

Action:

Institutional flows favor Nasdaq and Midcaps over broad SPX exposure.

Leveraged Fund shorting in NDX/RTY creates potential squeeze risk if growth momentum persists.

Lower VIX shorts suggest some reduction in vol complacency, but not yet a major risk-off signal.

The flow message is clear:

Investors are not de-risking equities broadly — they are rotating aggressively.

They are buying:

Memory/Semis

Tech

Discretionary

Financials

Healthcare

Staples

IG credit / aggregate bonds

They are selling:

Energy

Materials

Gold

Broad commodities

Crypto

Generic AI thematic funds

Long-dated rates via futures

Best trading expression

Long Memory/Semis + quality Tech/HC/Staples vs. short Energy/Materials/Gold/Crypto.

Key risk

ETF rebalance/CIB noise is still distorting factor flows, so avoid over-reading Growth/Value redemptions. The cleaner signal is sector/thematic: AI infrastructure is still being bought, geopolitical hedges are being sold.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!