S&P500 Trading Update 12/5/26

S&P500 Trading Update 12/5/26

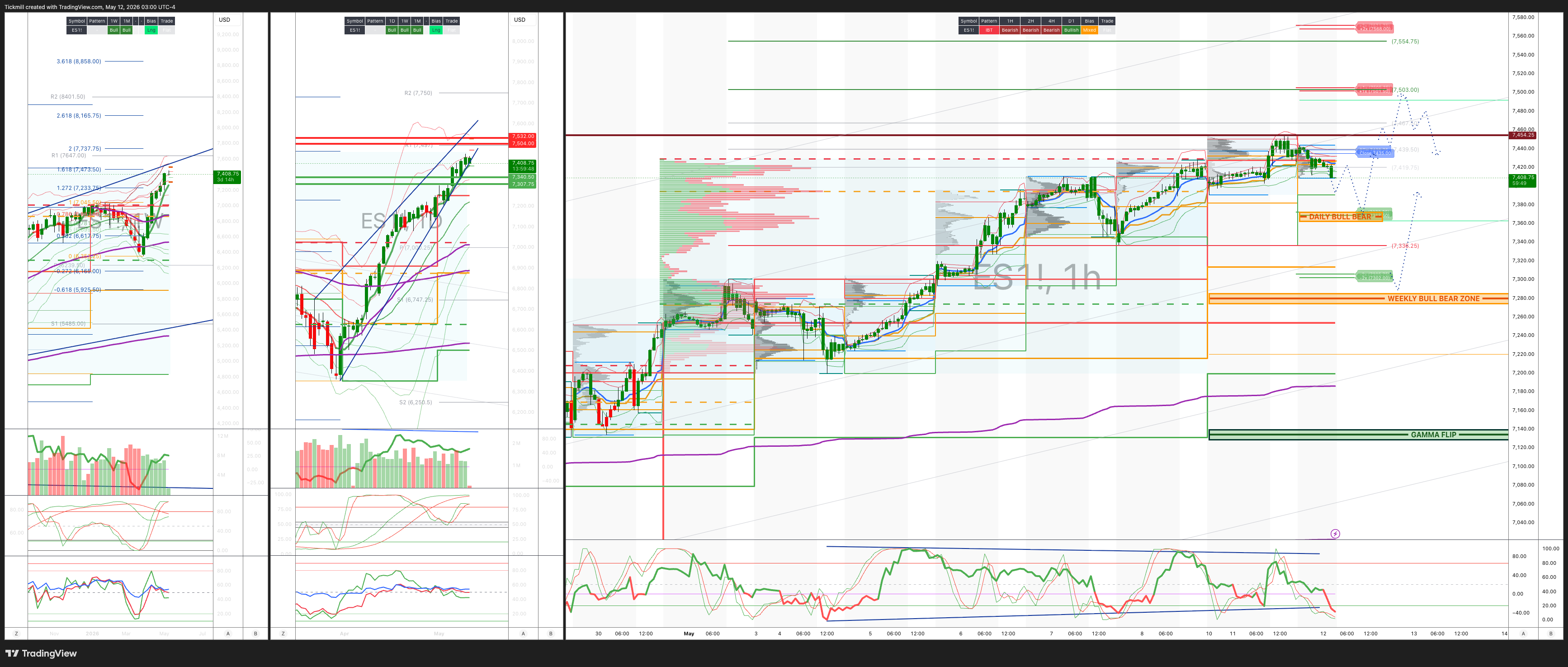

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7280/70

WEEKLY RANGE RES 7356 SUP 7138

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.27 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7398

WEEKLY VWAP BULLISH 7255

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFH - 7410

WEEKLY STRUCTURE – OTFH - 7199

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7360/70

GAMMA FLIP 7135

DELTA FLIP 6932

DAILY RANGE RES 7501 SUP 7372

2 SIGMA RES 7568 SUP 7305

VIX BULL BEAR ZONE 19.5

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET RTH CLOSE > DAILY/WEEKLY RANGE RES

LONG ON REJECT/RECLAIM WEEKLY BULL BEAR ZONE TARGET 7394

SHORT ON REJECT/RECLAIM DAILY/WEEKLY RANGE RES TARGET 7455

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Retail’

US Close: Risk-On Price, Risk-Off Internals

US equities finished modestly higher, but the session was much less constructive under the surface. S&P +19bps to 7,413, NDX +29bps to 29,321, R2K +33bps to 2,871, and Dow +19bps to 49,704, with a +USD 1.8bn MOC buy imbalance. Volumes were elevated at 21.5bn shares, well above the 19bn YTD average.

The cross-asset backdrop was not especially supportive: VIX +692bps to 18.38, WTI +331bps to USD 98.58, 10Y +6bps to 4.41%, gold +42bps to USD 4,735, DXY +6bps to 97.96, and Bitcoin +148bps to USD 81,913. Equities managed to close higher despite reports that the US-Iran ceasefire may be on hold, which pushed oil, rates and vol higher. This was another version of the recent spot-up / vol-up regime: the index can grind higher, but investors are increasingly willing to pay for protection or event convexity.

Tape: Narrow Breadth, AI Still Carrying the Market

The headline index gains masked narrow breadth. Leadership was concentrated in AI / high-velocity pockets, helped by reports of a potential Samsung union strike, which supported memory and semi-supply chain scarcity narratives. That fits the broader recent pattern: the market is still willing to chase AI infrastructure beneficiaries, especially where there is a perceived supply constraint.

But the quality of the move was weaker than the index close suggests. The desk described the session as choppy, with muted risk appetite and low overall activity. The floor was only 3/10 in activity levels and finished -166bps for sale versus a 30-day average of +157bps to buy. Asset managers were slight net sellers, led by macro, industrials, healthcare and financials. Hedge funds were roughly flat.

The key point: this was not broad-based institutional risk accumulation. It was more of a selective AI/momentum grind with investors cautious elsewhere.

Semis: Fervor Is Building Again

The semi tape remains powerful but increasingly speculative. The desk flagged several signs of rising heat:

Record call volumes in memory.

Asset growth in leveraged sector ETFs.

Institutional short covering in heavily shorted names.

QCOM and INTC short interest at multi-year highs into the rallies.

Semis now the largest constituent in flagship momentum baskets.

That does not mean the trade is done. But it does mean the character of the move is changing. Earlier in the rally, the setup was more fundamental: earnings, guidance, AI capex, memory pricing and supply-chain diversification. Now there are more signs of forced buying, short covering, levered ETF demand and factor chasing.

That is still bullish while it lasts, but it raises the risk of sharper air pockets if the catalyst stream slows or if rates/oil move against the trade.

Retail: Worst Day Since 2022

The weakest area was retail, which had its worst day since 2022. The pressure reflects a combination of factors:

Consumer anxiety after MCD, SHAK and PLNT commentary last week.

Ongoing rotation into TMT.

Stubbornly high gasoline prices.

Concerns around Hantavirus headlines.

Lack of generalist sponsorship.

Weak sentiment around lower-income discretionary demand.

This lines up with the broader macro framework: high gasoline prices are a direct tax on lower-income consumers, and restaurants/retail are where that pressure shows up quickly. The market had been willing to squeeze consumer names on de-escalation hopes and lower oil days, but with crude back near USD 99, the squeeze case is less clean.

Near-term, the GS Staples Forum could matter for read-throughs on pricing, volumes, trade-down behavior and margin resilience. But for now, retail looks like the clearest loser from the oil/rates/geopolitical mix.

Bitcoin Sensitives: Legislative Optionality

Bitcoin-sensitive equities outperformed, with investors focused on the potential CLARITY Act markup and possibly a floor vote as soon as this week. Momentum seems to be improving, especially with the COIN CEO now tweeting in support despite not supporting prior versions.

That said, the desk rightly notes that this is still a long way from becoming law, similar to the housing bill dynamic. So the trade is about legislative optionality and sentiment rather than near-term fundamental certainty.

The clean read: crypto equities can continue to catch a bid on policy momentum, but the risk is that expectations move faster than the legislative process.

Vol: Spot-Up / Vol-Up Continues

Derivatives were steady but important. Vols rose across all three major indices, continuing the spot-up / vol-up pattern. This is not typical calm bull-market behavior. It suggests investors are happy to hold upside exposure but want to own convexity around the next event window: Iran, Trump’s China trip, CPI, Fed path and AI earnings.

The desk thinks NDX vol looks especially high and sees short gamma as attractive. The straddle for tomorrow went out around 52bps, suggesting the market is not necessarily worried about immediate realized moves but is uncomfortable with implied vols continuing to rise.

The key line is that the market appears to imply fears may not fully materialize until after President Trump’s China trip. That supports continued positive correlation between spot and vol: equities can rise as investors also buy vol, because the market is climbing into unresolved event risk rather than away from it.

Fed: Cuts Pushed Further Out

GIR pushed back the final two Fed cuts in its forecast by one quarter, to December 2026 and March 2027. The logic is straightforward: energy cost passthrough is likely to keep year-over-year core PCE closer to 3% than 2% for much of the year.

For the FOMC to cut this year, GIR now thinks the market needs both:

Lower monthly inflation prints after the oil shock fades.

Further labor-market softening.

They still expect that bar to be met, but later than before. This is important because it limits the degree to which equities can rely on near-term Fed relief. It also explains why higher oil and higher yields are such an important macro ceiling for the market.

Trading Takeaways

The headline index close was fine, but the internals were more fragile. This remains a market where AI momentum can pull the index higher even as vol, oil and yields rise, but that is not a stable broad-risk setup.

The best long remains selective AI infrastructure, especially where supply constraints or memory/power/data-center bottlenecks support pricing. But the semi trade is showing signs of speculative heat, so fresh exposure should be more tactical: call spreads, relative value, or buying pullbacks rather than chasing vertical moves.

Retail and lower-income discretionary look vulnerable again. The combination of high gas prices, weak restaurant commentary, consumer anxiety and rotation into TMT makes the group a better funding short than a clean long, unless oil breaks lower again.

Vol remains tricky. Broad index vol is not obviously cheap after the move higher, and NDX vol may be elevated, but the spot-up / vol-up regime argues against being casually short convexity across the board. Better to be selective: fade overextended NDX gamma where rich, but keep event hedges around Iran, China and CPI.

Bottom line: the market is still going up, but it is doing so on narrower leadership, higher vol, higher oil and higher yields. That argues for staying long the secular winners, reducing exposure to weak cyclicals/retail, and avoiding complacency on macro hedges.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!